Software for Hardware → Hardware like Software

How AI is changing the development process of mission-critical automation systems

Within the venture community it has historically been said that “hardware is hard.” For the record, I’ve never liked this saying. I find it both vague (as an investor) and wimpy (as a roboticist). Nevertheless, there are undeniable challenges when developing a complex physical product—supply chain management, hardware debugging, development costs, lengthy timelines, and recruiting a team with niche yet multidisciplinary expertise, just to name a few.

But with falling hardware costs and continued improvement in AI solutions, the software layer is finally becoming strong enough to take meaningful weight off engineers who are building mission-critical systems up and down the stack.

In my view, the right question isn’t whether AI can fully design an airplane wing assembly or write flight-control firmware from scratch. The more relevant question is:

“Which sub-tasks in the hardware development lifecycle is AI robust enough to tackle on its own? Where does AI adoption yield immediate, quantifiable wins without compromising safety or reliability?”

Having recently backed a stealth company in this category (more on that in a few weeks!), I can confirm that there is a market – ready today – that validates this thesis with numerous use cases of AI-powered software finding traction in hardware development.

Let’s dive in.

Why Now? Four Major Shifts Converging

1. Sim & synthetic data as the logical “first step.”

With broader access to simulation toolkits, modern robotics startups are moving sim-first. The “new way” of building robotics is: simulate → generate data → validate → deploy.

Teams now design, test, and validate behaviors in physics-based virtual environments (anchored for now by NVIDIA Omniverse). Many even bootstrap models with synthetic data before touching hardware. This workflow lets engineers harden products against noise, drift, and real-world variability—even when (and especially important for) using inexpensive components.

2. Industrial data finally getting connective tissue.

Brownfield plants have SCADA/PLC signals, historians, cameras, MES, and SQL—each useful but largely isolated. Today, engineers manually overlay and cross-link these data streams to derive insights. New Industrial DataOps tools now sit between OT and IT systems to model, govern, and contextualize data, moving it into modern analytics/AI pipelines. In practice, AI-powered integrations are giving SCADA a facelift (and a jetpack), allowing manufacturers to finally reap the benefits of AI-driven operational insights.

3. Autonomy is becoming a software business model.

We’re seeing, and will continue to see, an accelerating decoupling of hardware and software for autonomy across manufacturing, energy, mining, and defense, as the technologies of each mature. This shift opens the door for horizontal software winners even as hardware itself commoditizes, opening the door for horizontal solutions to become the go-to /drag-and-drop product engineers use to tackle recurring challenges and bottlenecks across industries.

4. Capital is re-orienting to full-stack industrial plays.

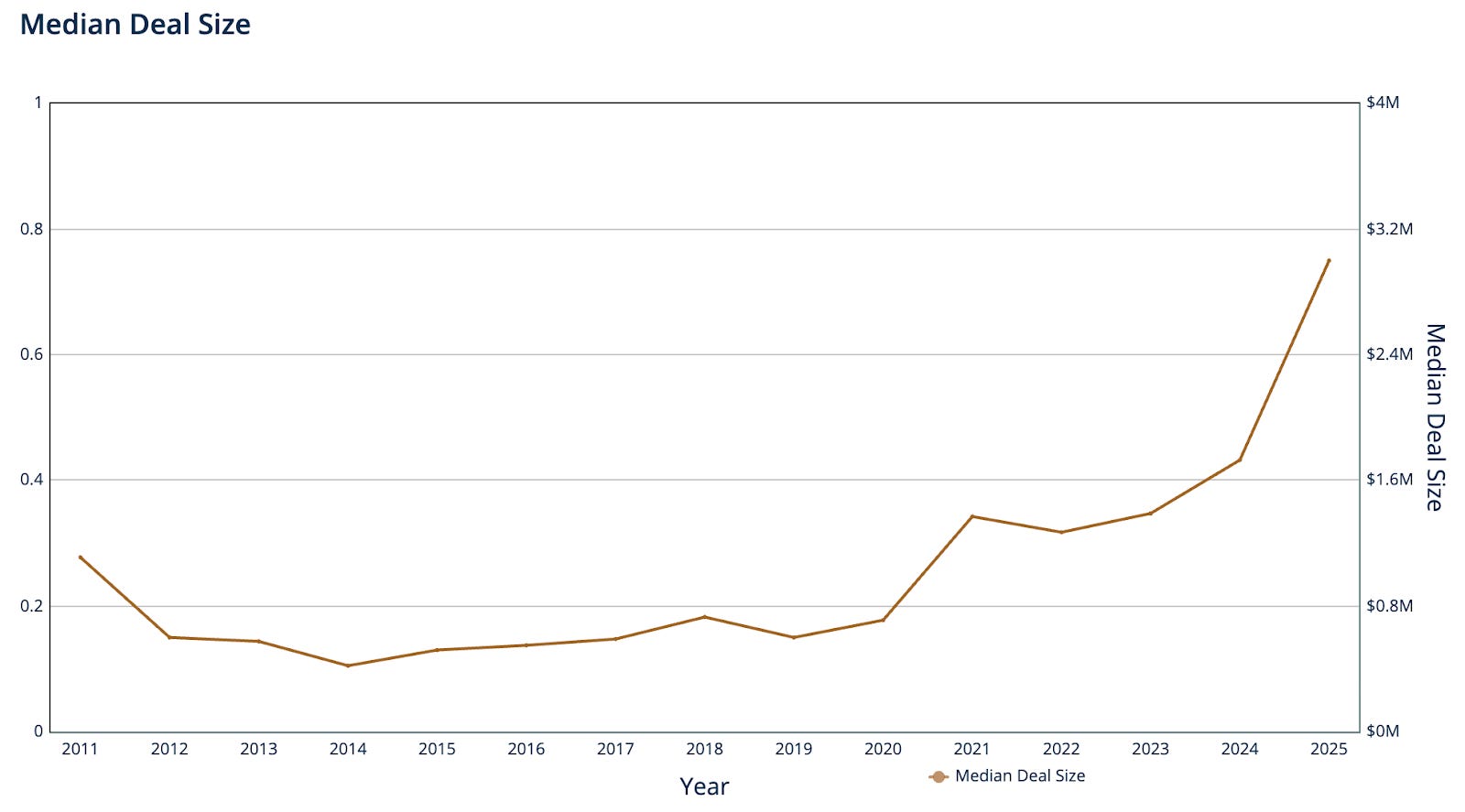

Read as: “Deep Tech & industrial VC is cool now 😎🤘🏾” Deep tech investment is on track to exceed $84B in 2025, up from $65B in FY2024. Median deal size is up 73% year-over-year to $3M from $1.73M (PitchBook). The narrative is moving past “hardware is hard” toward “software-defined physical systems,” with data as the compounding moat.

What We’re Looking For in the Emerging “Software for Hardware” Layer

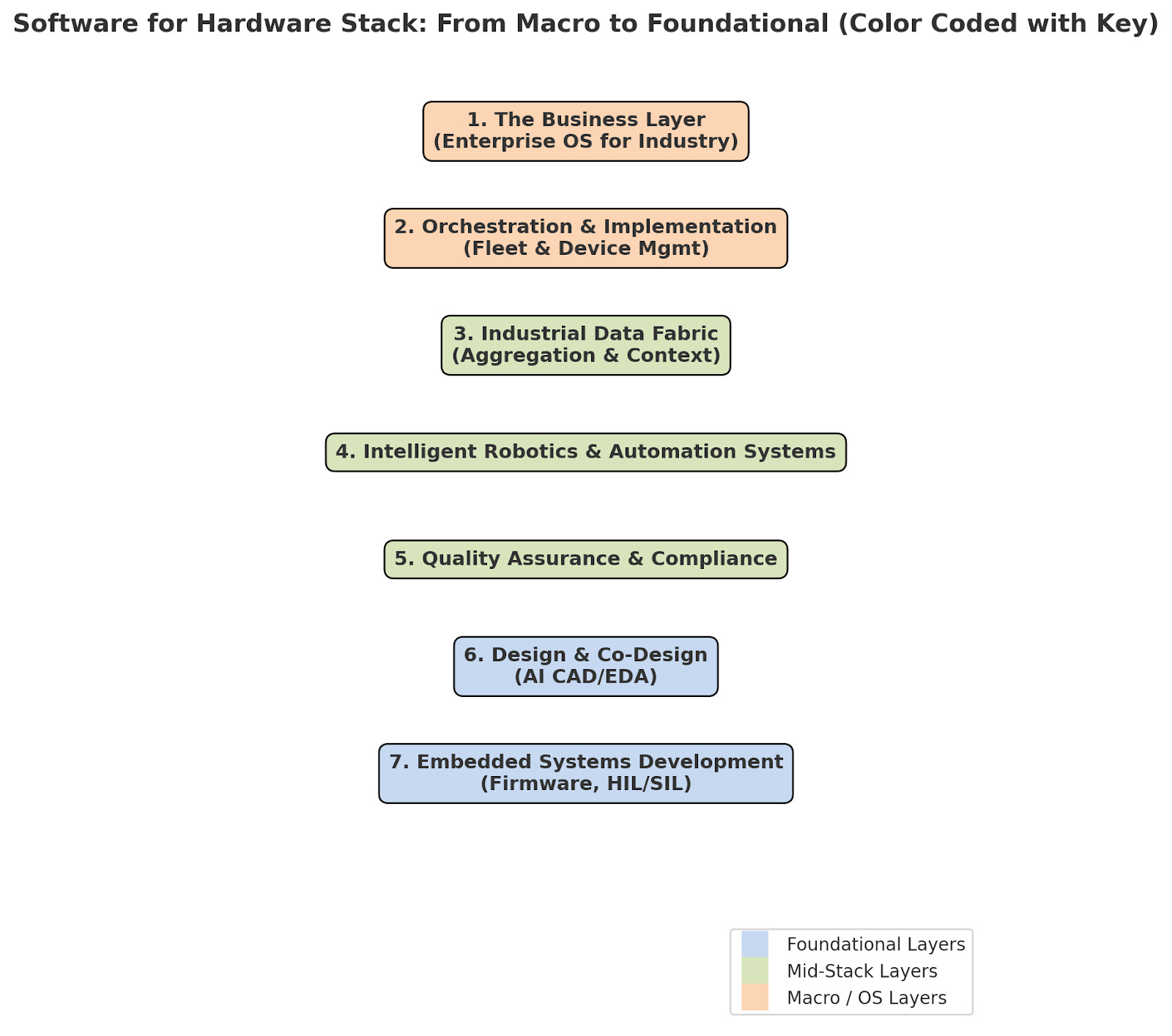

I like to think of the stack in seven investable and mutually reinforcing layers, organized from the highest-level “macro/OS/business” layer down to the lowest-level foundational tooling.

1 - The Business Layer

Industrial customers (factories) are businesses first—and yet their administrative systems are, in large, shockingly outdated. AI can streamline these processes and these customers are looking for this kind of low-hanging-fruit ROI.

What we are looking for:

Complex machine procurement platforms and marketplaces

Intelligent BOM and component selection for cost and supply chain risk management

AI-powered financial tools (capital equipment financing, insurance, compliance)

2 - Orchestration & Implementation (Fleet & Device Mgmt, Live Updates, Data Movement)

Poor implementation is (still) the #1 failure mode for automation deployments today. Cross-hardware, swarm level, orchestration and a unified data plane are prerequisites for reliable fleet operation. These systems get data from the physical world to the cloud, and act back on it in real time.

What we are looking for:

Systems of record and intelligence for lights-out factory management

Topology-agnostic robot fleet management and coordination

3 - Industrial Data Fabric (Aggregation, Context, Governance, Observability)

This layer normalizes SCADA/PLC/video/ERP/MES into a single, time-aligned, queryable model (think data ops + historians + cloud services). With it, production lines can be measured, optimized, and adapted in near-real time to ensure reliable production.

What we are looking for:

Capturing and retrieving institutional industrial knowledge from operators and machines

The “Scale AI” for manufacturing → data cleaning, labeling, and structuring across silos

4 - Intelligence for Robotics & Industrial Automation Systems

Everyone’s favorite - Human-like intelligence for robotic automation. This group of technologies is designed to address projected labor shortages and associated productivity decline. These investments are heavily AI-enabled and financially promising, but face *very* steep technical challenges, and remain highly capital intensive. Robotic intelligence is currently constrained by limited controls data, siloed industrial operations data, and rapidly evolving model architectures. Until these bottlenecks are solved, these systems remain less reliable than human operators or classic automation.

What we are looking for:

Semi-autonomous systems with human-in-the-loop oversight and manual override

Simulation & digital twin infrastructure with proprietary data ingestion pipelines and high-fidelity environments

Verticalized robotics plays that prove ROI by becoming their own customer and delivering value in mature industrial markets

Real-world controls data capture: making it nearly free to log, curate, and reuse teleop traces, exception recoveries, and human corrections for training

5 - Quality Assurance & Compliance

Every complex system undergoes rigorous testing, but inspections are costly and often batched. Regulated industries (aerospace, defense, energy) can’t tolerate compliance failures, so they overspend on testing and validation. Ironically, the better the process, the less likely inspections catch errors—making them more wasteful overall.

What we are looking for:

AI-powered automated inspection, NDE assistance, root cause analysis

AI-generated manufacturing work instructions

6 - Design & Co-Design (AI CAD/EDA, Auto-Selection, Verification)

Generative design tools that parse requirements, schematics, and datasheets, propose designs & layouts, pick components, and generate first-pass code — all parameterized for easy user modification, standardized outputs, and simplified manufacturing.

What we are looking for:

Design-space exploration in EDA (chip/FPGA/ASIC)

Vertical-specific CAD/CAM design tools

Hardware design collaboration, revision tracking, and control

7 - Embedded Systems Development (Firmware, Drivers, HIL/SIL, etc.)

Every smart device has a controller, which implies that a truly shockingly large amount of engineering time is spent on embedded systems. Initializing and testing hardware is critical (to ensure functional designs) but repetitive and mundane — It is exactly the kind of work AI can streamline, to free engineers to focus on strategic design.

What we are looking for:

Embedded software toolchains (firmware scaffolding, compilers, debuggers, IDEs)

Verification & validation (SIL, HIL, unit testing, model-based testing, coverage closure)

Going to Market

Manufacturing is a great entry point for software-for-hardware. The installed base is huge, pressure to prove ROI on CapEx is prevalent, and data feedback loops are fairly well developed. Amazon-scale players often lead in piloting new capabilities, but in my view, the bigger opportunity is democratization—making intelligence and software tools available for the other 80% of manufacturers that are not yet automated.

Fair warning - most legacy OEMs are skeptical of AI, but this is not a unique or unexpected response. Finance and healthcare were, too, in the early days of software adoption until the systems showed their value. Successful entrant companies start with a focused pain point, prove reliability, integrate cleanly with existing systems, and then expand to win over time. And once manufacturing enterprises adopt, they tend to stick, and the switching costs work in your favor.

The Cumulative Effect of Investing in the Category

AI and software tools speed up hardware iteration cycles. Faster loops mean better decisions, earlier. Hardware gets into the field faster, producing real-world feedback sooner—the most critical part of the cycle. Great tools shorten the time to generating high-quality, high fidelity, information.

This is a massive enabler of innovation, unlocking the creativity of engineers as builders. Most teams operate under intense time and budget pressures, which discourages exploration and leads to an accumulation of technical debt from unresolved inefficiencies (rather than discovering an OOM better design). In my experience, unrestricted experimentation is the difference between feeling stuck and feeling alive as an engineer.

Anecdote: When I was at SpaceX, we spared no expense (...no expense) to try multiple solutions in parallel— It was costly, but essential for finding the very best answer as quickly as possible. AI has the potential to make that style of parallelism economically accessible to far more hardware companies - and ultimately this creative unlock raises the odds of reaching the optimal configuration. It’s like The WD-40 story (anecdote #2 😅): it took 39 failed formulas before they landed on the 40th - more enabled attempts, means better solutions (imagine if we only got to WD-39 because the lab ran out of time).

We care about industrial productivity and human flourishing. We need world-class software tools embedded in the hardware development process. And at AlleyCorp we’re excited to back the next generation of transformative companies building exactly that. If that is you, please reach out to us!